Managing your income effectively is crucial for maintaining financial stability and achieving your long-term goals. One key aspect of financial management is allocating your income to different expenses. While there is no one-size-fits-all answer to what percentage of your income should be allocated to each expense category, there are some general guidelines that can help you create a balanced budget.

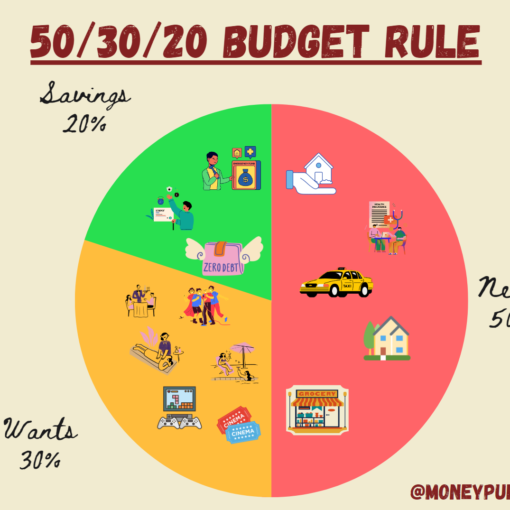

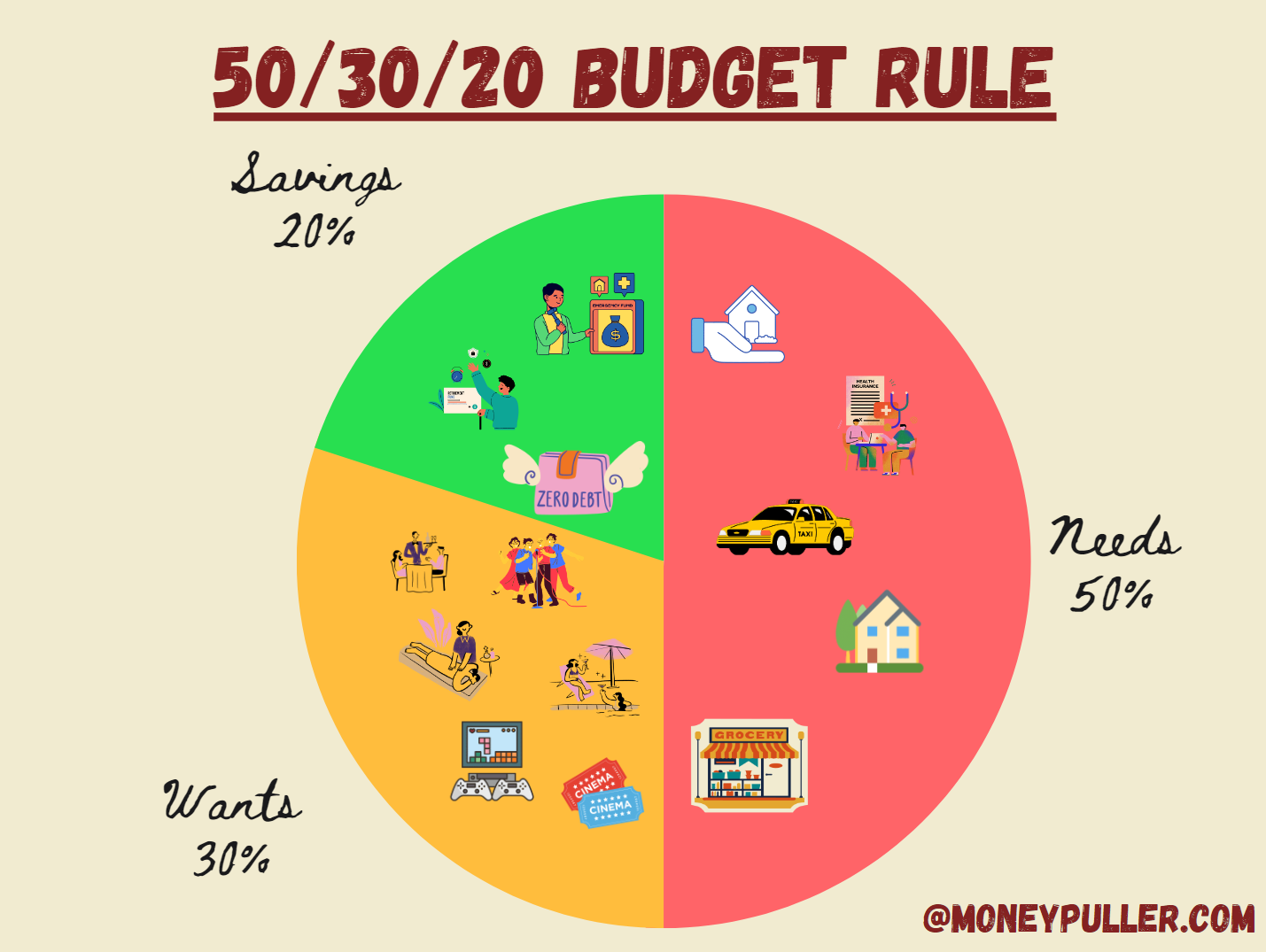

1. Fixed Expenses: 50%

Fixed expenses are recurring costs that remain relatively stable from month to month. These include rent or mortgage payments, utilities, insurance premiums, and loan repayments. As a general rule, aim to allocate around 50% of your income to cover these fixed expenses.

For example, if your monthly income is $4,000, you should allocate approximately $2,000 for your fixed expenses. This ensures that you have a stable foundation for your budget and can meet your essential needs without financial strain.

2. Variable Expenses: 30%

Variable expenses are costs that fluctuate from month to month and are more discretionary in nature. This category includes groceries, dining out, entertainment, clothing, and personal care. Allocate around 30% of your income to cover these variable expenses.

Using the same example, you would allocate $1,200 (30% of $4,000) for your variable expenses. This provides flexibility for you to enjoy some discretionary spending while still maintaining financial discipline.

3. Financial Goals: 20%

Allocating a portion of your income towards your financial goals is essential for long-term financial success. This category includes savings, investments, debt repayment, and building an emergency fund. Aim to allocate at least 20% of your income towards your financial goals.

In our example, $800 (20% of $4,000) would be allocated to your financial goals. This allows you to save for the future, pay off debts, and build a safety net for unexpected expenses.

Customizing Your Allocation

While the 50-30-20 guideline provides a useful starting point, it’s important to customize your allocation based on your individual circumstances and priorities. Here are a few factors to consider:

1. Income Level

Your income level plays a significant role in determining how much you can allocate to each expense category. If your income is limited, you may need to adjust the percentages accordingly.

2. Financial Obligations

Consider any specific financial obligations you have, such as child support, alimony, or student loan payments. These obligations may require a larger portion of your income to be allocated to fixed expenses or debt repayment.

3. Lifestyle Choices

Your lifestyle choices and priorities will also impact your allocation. If you enjoy dining out frequently or have expensive hobbies, you may need to allocate a larger percentage to variable expenses. Similarly, if you prioritize saving for a down payment on a house or early retirement, you may choose to allocate more towards your financial goals.

4. Geographic Location

The cost of living varies significantly depending on your geographic location. If you live in an area with high housing costs or a higher overall cost of living, you may need to allocate a larger percentage to fixed expenses.

Regular Evaluation and Adjustments

Remember, budgeting is not a one-time task. It requires regular evaluation and adjustments. As your income or expenses change, revisit your allocation and make necessary adjustments to ensure your budget remains balanced and aligned with your financial goals.

By allocating your income wisely, you can achieve a healthy financial balance, meet your obligations, enjoy some discretionary spending, and work towards your long-term financial goals. Remember, these guidelines are just a starting point, and it’s important to customize them to suit your individual needs and aspirations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}